Export accompanying document

Information on the creation of the export accompanying document

The export accompanying document (EX.1 or EAD) is a document that accompanies the goods to be exported from the country. More precisely, goods that are usually exported commercially from Germany to a so-called third country, i.e. a non-EU country, e.g. goods that are shipped by truck to Switzerland or by ship to the United States. The ABD then accompanies the goods to the external EU border, i.e. to the port or national border of the third country. Up to a goods value of EUR 1000 and a weight of 1000 kg, no export accompanying document is required. However, if one or both of these values are exceeded, such a document is mandatory for commercial transactions. In principle, the following applies to every cross-border transportation process: the goods have to be deregistered from the country they are leaving (=export) and registered in the country they are going to (=import).

The export accompanying document therefore ensures the deregistration of the goods from Germany. However, in order to speed up the processes and simplify them for the customs offices, for some years now this procedure has only been possible online via a direct interface to customs with often expensive software and corresponding expertise. But an interface is not enough to create an export document such as the ABD. It may be necessary to check whether the export is subject to authorization or whether the goods may not be exported to the country in question at all.

that does not belong to the European Union, an ABD must be created.

(EU countries here in orange on the map)

Introduction - ABD

If you want to export goods to a non-EU country for the first time, you will probably have heard the term Export Accompanying Document (EAD) before. But what exactly is it all about and how does the export accompanying document work on the one hand and what is the procedure after the document has been created on the other?

Structure of the export accompanying document

Below you can find out what data we need from you to create the export accompanying document (ABD). You will gain a more detailed insight into the structure of the German export declaration. This can help you to better understand the connections and information.

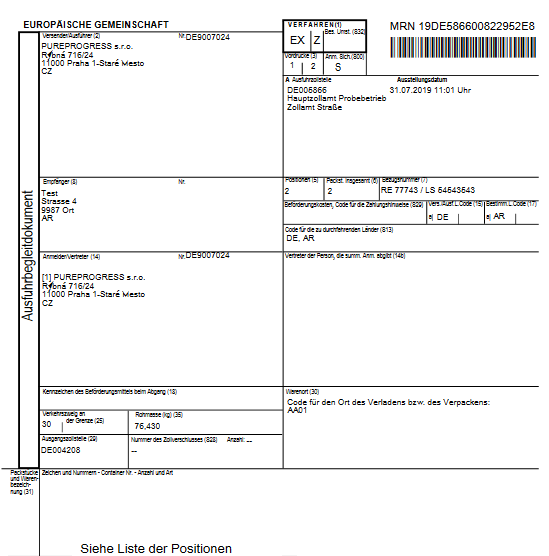

Sample export accompanying document

To give you a better idea, we have created a sample export accompanying document for you here. The finished document would then look something like this after we have created it for you (see below). Please note that this preview is only the first page of the document. If you click on the preview image, the complete document will open in a new window. You can then download the PDF document if required.

However, not all fields of the ABD need to be completed in your specific case. So which information is always required and which is only needed in special cases?

Click on the image to open the full document

Participant constellation

Let’s first take a look at the document provided in the example (see link above). The structure of the export accompanying document is always the same: it lists the parties involved in the transaction and details of the goods.

Let’s start at the top left, with the Shipper/Exporter field (field 2). To understand why it says sender and not sender, it is first important to know the following. In the forwarding business, the shipper is the party who actually ships the goods or from where the goods are originally shipped. For example, the goods are shipped from a company in Hamburg to New York. The forwarder/transporter is based in Bremen, so he is the sender. The company in Hamburg is therefore the sender. The sender here would be the forwarding company in Bremen. However, the Export Accompanying Document (EAD) does not simply say “consignor”, but “consignor/exporter”. It is therefore important to know that the exporter is the person who assumes responsibility for the export of the goods (more on this here).

To return to the above example, let’s assume that the goods are located at a company in Hamburg. Although the company ships the goods, it only acts on behalf of a company in Belgium. Ultimately, the company wants to ship the goods to New York. The exporter is authoritative. In this case, this is the company in Belgium, which must be entered in the corresponding field. However, the company in Hamburg, where the goods are actually located, will not appear in the document. However, this does not mean that customs does not still want to know where the goods are located. They may want to take a closer look at the goods and check whether they are the goods declared.

EORI no. (customs number)

The address of the exporter is therefore required on the one hand, and the loading address on the other (company name + address in each case). You also need an EORI number for the recipient’s address. This serves to enable customs to identify the person involved under customs law. Without this, no export is possible if you are trading commercially. You can apply for an EORI number free of charge from German customs at www.zoll.de.

Let’s move on to the next field, the consignee field (field 8), directly below the “Consignor/exporter” field. Enter the name and address of the actual consignee here. Under “No.” you can again enter the EORI number of the consignee, if they require one. However, this is not absolutely necessary as, for example, a company outside the EU does not usually have an EORI number.

In the declarant/representative field below (field 14), you will see the address of the person who made the customs declaration. If you register yourself, your own address will appear here. Otherwise, the address of the customs agent is shown here, as they represent you.

Means of transportation and weight

Enter the license plate number of the truck transporting the goods in field 18 “License plate number of the means of transport at departure”. This field is not mandatory. Often the license plate number is not even known to the sender at the time of registration.

Field 25 indicates the mode of transport at the border. This means whether the goods are transported by truck, airplane, ship, etc. – Here “33” stands for truck transportation.

Field 35 represents the “gross weight” of the goods (in kilograms). The gross weight is the total weight of the goods incl. of any packaging and pallets.

Customs offices involved in the procedure

Box 29 indicates the customs office of exit, i.e. the customs office where the goods leave the EU. This can be, for example, a customs office at the border with Switzerland or at a port.

Do not enter anything under “Number of customs bond”, field S28, as customs may fill this field in themselves. This guarantees the so-called identification of the goods. You can find out more about this topic in our other article on the various customs procedures.

This means that we have completed / processed the left half of the first page of the Export Accompanying Document (EAD) together.

In the right-hand column, we see the export procedure in field 1 (more on this here). This can be, for example, the export of the goods from the EU or export to an EFTA country, etc. – and any special circumstances in field S 32.

In field 3 “Forms” we see the number 1 on the left and the number 2 on the right. This information shows how many pages the document contains. In this case, this means that we are on page 1 of a total of 2 pages.

Field S00 is completed if security-relevant data is transmitted with the export. This is therefore irrelevant for us, as it is filled in automatically.

Structure of the MRN number + additional information

At the top right you will see the MRN number, i.e. the Movement Reference Number. It corresponds to a code for tracking the document. Similar to tracking a parcel shipment, each interface, i.e. each border, scans the document. This makes it possible to trace exactly where the goods left the EU.

The MRN is structured as follows. 19 (the number of the year, in this case 2019), DE for the country and then the first 4 digits of the customs office that issued the ABD. This means that 19DE586600822952E8 stands for an export accompanying document (ABD) from 2019, which was released in Germany by the customs office with the number 5866. The following numbers are a sequential number and a calculated control number.

Field A, directly below, again shows the customs office incl. Address and date of issue.

Field 5 shows the number of customs items, i.e. how many different types of goods the consignment contains. You can see the number of packages in the shipment in field 6, for example “10” for a total of 10 pallets of goods. The internal reference number of the customs service provider for this consignment / declaration appears in field 7.

All other fields on the first page are automatically filled in and therefore require no further explanation.

Customs positions: Description of goods and customs tariff number

In field 31 at the bottom of the page, the goods are now normally named exactly. However, as this is a detailed description of the product, the text module was too large to be included on the first page. All items and goods can therefore be found on page 2.

There you will find a detailed description of the goods incl. Gross/net weight and customs tariff number and procedure.

To create the ABD, we therefore also need the exact customs tariff number, the description of the goods, weights and documents such as the invoice and delivery bill, as shown on the ABD.

You are welcome to send us an e-mail in advance to [email protected] or give us a call so that we can discuss together which documents you need. We look forward to hearing from you!

Is there a customs form for the export accompanying document?

We are repeatedly asked whether it would be possible to simply fill out the export accompanying document at customs yourself, e.g. using a form. Unfortunately, since 2009 it has only been possible to create the document electronically. This requires special software in which the entries can be made. Only in exceptional cases, such as a system failure or a technical malfunction of the German customs servers, may the declaration still be made on paper. Even then, the electronic form must be submitted later.

How does the export accompanying document work?

The export accompanying document is usually prepared by a customs service provider such as us. This declares the goods to be exported to customs via an electronic interface. With the transmission, he therefore submits an application for release of the goods and release of the export accompanying document. If the responsible customs office approves the export, a PDF document is created. In order for the goods to be released, they must generally be declared at the customs office responsible for the place of loading of the goods in accordance with the customs regulations. is responsible for the official directory. Depending on the zip code, a different inland customs office may therefore be responsible for the loading point in the external warehouse than for the company’s headquarters.

The export accompanying document contains information on the consignor of the goods, the consignee of the goods, the goods themselves and the export procedure.

In order to identify the companies involved for customs purposes, they must have a so-called EORI number, which can be applied for at German customs.

What happens after the ABD has been created?

After your customs service provider has declared the export to the respective inland customs office, the goods are released immediately (goods value up to EUR 3000) or after a so-called presentation period (goods value from EUR 3000), depending on the value of the goods. During this presentation period of 24 hours, customs has the option of inspecting the goods on site and checking the information you provided in the export declaration. This also means that the goods may not yet be loaded during this time and may not be removed from the place of loading specified in the export. After the 24-hour period has expired, you will receive customs clearance for export. Your customs service provider can then print out your export accompanying document or send it to you by e-mail so that you or your carrier can transport the goods to the border.

The export accompanying document is then scanned at the external EU border. For this purpose, there is a barcode on the export accompanying document, a so-called Movement Reference Number, also abbreviated to MRN. Movement Reference Number literally means movement reference number. This number can therefore be used to trace which borders the goods have passed through at any time. Sometimes the MRN is mistakenly equated with the ABD. However, this is not correct, as the MRN is only a number that is part of the export accompanying document and other export documents, such as T1 or T2 documents, also have such an MRN.

Once the export accompanying document has been scanned by the border customs office, the document is automatically converted into an exit endorsement. This completes the process. The exit note serves as proof that the goods have actually left the country. You therefore need this exit note to prove during a tax audit that the goods were not sold within Germany (subject to VAT) instead of abroad (VAT-free).

The status of each export accompanying document, i.e. whether the document has already left the EU, can be checked under the following link: Tracking an export MRN

Do you have any questions?

We will be happy to help you apply for an EORI number, prepare the export accompanying document and let you benefit from our many years of expertise. Simply give us a call or send us an e-mail.

Further help and information on the Export Accompanying Document can be found further down on this page or in our specialist articles on the Export Accompanying Document. We have summarized the most common explanations of terms for you in our customs glossary.

We are also happy to help with other customs-related issues. ==> To our prices

Which documents must be provided to customs, do the goods have to be presented to customs, etc.?

We will be happy to advise you!

The creation of the export accompanying document is the first step towards the successful export of your goods.

With us, you have a reliable partner at your side!

If you export goods more frequently in the future, we can offer you particularly favorable conditions and exclusive benefits.

What is the export accompanying document?

The Export Accompanying Document (EAD) is the written proof that the export of certain goods is permitted. You may therefore export the goods listed in the document from the European Union. You can then transport the goods to an EFTA country (e.g. Switzerland) or a third country. Sometimes the export accompanying document is also referred to synonymously as an export declaration or export declaration.

Since 01.07.2009, this declaration is only possible electronically via ATLAS (Automated Tariff and Local Customs Clearance System). This has replaced paper-based registration. Depending on the constellation of the parties involved in the legal transaction and the weight and value of the goods, an electronic export declaration is mandatory in some cases and not necessary in others.

The export accompanying document consists of the details of the parties involved, the procedure and the goods. Using a unique 18-digit tracking number (MRN = Movement Reference Number) in the form of a barcode, it is possible to trace at any time at which EU customs office the goods were cleared. As soon as the customs office at the EU external border scans the export accompanying document, it generates a so-called exit endorsement. This is proof that the goods have been properly exported from the EU.

The information in the ABD is used to record the flow of goods and is included in the foreign trade statistics published by the Federal Statistical Office. With the help of the ABD, it is possible to check whether the exporter is complying with export regulations and foreign trade law.

When is an export accompanying document required?

To export goods from the EU to an EFTA/third country, you must always create an export accompanying document for goods with a value of EUR 1,000 or more and/or a weight of over 1,000 kg. However, if you export the goods as a private individual and transport them yourself, some customs offices do not issue an export declaration. However, it is always better to arrange the export in advance to avoid difficulties at the border.

You therefore need an export accompanying document if

- The goods leave the EU* and

- the value of the goods is over 1000 EUR or

- the weight of the shipment is over 1000 kg

*= If, for example, the goods leave the customs union for a short time, as in the case of a shipment from Spain to the Canary Islands, you will also need an export accompanying document.

We already explained how the export accompanying document is structured in our last article in the online help for the ABD. We will now show the differences between the various export accompanying document procedures.

There are basically two different procedures. The so-called one-stage procedure and the two-stage procedure. Depending on the procedure, different conditions apply in order to obtain export clearance.

The one-step procedure

Up to a value of EUR 3,000, the single-stage export accompanying document procedure must be used. The customs agent sends a declaration via ATLAS to the customs office of export. The customs office of export always corresponds to the inland customs office at the seller’s location. If the goods are located in a different place, you must declare the goods at the customs office of export responsible for the place of loading. In the single-stage procedure, however, this customs office of export also serves as the customs office of exit. The customs office of exit is always the customs office at the external EU border.

Example 1 for the single-stage procedure

Since this sounds very theoretical, here is an example: A German mail order company receives a large order from Switzerland in the morning (value: EUR 2,500, weight: 880 kg). Just a few hours later, the company has palletized the goods and can export them. To do this, it must make a declaration to the customs office itself or through a customs agency. A freight forwarder is to transport the goods on a pallet by truck across the Weil am Rhein / Basel border into Switzerland.

The Weil am Rhein Autobahn customs office therefore receives an export application electronically in advance via ATLAS software. The customs agency then automatically receives a document with a barcode number (MRN), which it forwards to the forwarding agent. The forwarding agent takes the goods to the Weil am Rhein border and presents the document with the barcode number of the export accompanying document. Customs at the German EU external border compares the goods on site with the declaration and releases the export. This completes the export.

Example 2 for the single-stage procedure

Here is another example. The same mail order company in Germany also receives an order in the morning for a parcel going to Brazil (value: 1100 EUR, weight: 20 kg). As the recipient of the parcel is different from the consignment to Switzerland in example 1, the seller must have a separate export accompanying document drawn up. The company commissions a parcel service provider to collect the parcel in the afternoon. At the same time, the sender asks the parcel service provider via which airport the goods will be transported to Brazil.

He informs his customs service provider that the goods are leaving Germany via Frankfurt Airport. The latter then creates an export application via ATLAS and sends it electronically to the relevant customs office. The customs office then accepts the declaration for the time being. The export barcode is available to the parcel service provider as a printout and to the customs office electronically. After the goods have been collected by the parcel service provider and before the goods leave the country via air freight, the Frankfurt Airport customs office clears the export. The export is therefore completed.

Summary of the single-stage procedure

In summary, it must always be a German customs office of exit. Up to a value of EUR 3,000, an export must be applied for via ATLAS. The export can theoretically take place immediately without any waiting periods due to the procedure.

However, if a company were to send more than one consignment (e.g. as several partial deliveries) on the same day to the same recipient, it can declare the goods together as one export. This would save the company additional costs for a further process by the customs agent.

The two-stage procedure

If the value of the goods exceeds EUR 3,000, you must always use the two-stage export accompanying document procedure. The customs agent must also send a declaration to the customs office via ATLAS. However, in this case, the latter does not send the declaration to the customs office of exit. Instead, the declaration is sent directly to the customs office of export. This is the inland customs office near the exporter. It is possible to find out which customs office is responsible for the respective zip code on the German customs website(Find export customs office).

The declaration in the two-stage procedure at the customs office of export includes the same information as the declaration in the one-stage procedure. However, the customs office of exit differs from the customs office of export in the declaration in the two-stage procedure. While the customs office of exit and the customs office of export are the same office for the one-stage procedure, this is not usually the case for two-stage exports. This is because customs offices of exit, i.e. customs offices at the external EU border, are not normally assigned to a specific zip code as a customs office of export (internal customs office).

In contrast to the single-stage procedure, the transporter cannot take the goods directly to the border. Instead, he must present the goods at the inland customs office. This can be done in two different ways. The forwarding agent takes the goods to the export customs office in Germany. Alternatively, his customs agent declares the goods one day in advance at the responsible inland customs office. It defines a two- to four-hour period for the following day. During this time, customs can visit the shipper at the place of loading. After the time period has expired, the customs agent automatically receives the export release.

Example 1 of the two-stage procedure

The following is an example of when the two-stage procedure applies. A car manufacturer in southern Germany wants to sell and ship several vehicles to a car dealership in Belarus. For this purpose, he provides his customs agency with the necessary documents. This determines which export customs office is responsible for the seller’s registered office based on the zip code of the loading location of the goods. In this case, the customs agency sends the declaration electronically to the inland customs office in Böblingen. At the same time, the customs agent agrees the transport route with the carrier. He therefore knows that the freight forwarder is transporting the goods via the S19 expressway, which connects Poland and Belarus. The customs agent therefore indicates the Kuźnica customs office in Poland as the customs office of exit.

However, the vehicles will not be exported until the next few days. The car manufacturer therefore informs the customs agent that customs can come the following day between 10.00 – 14.00. The next day, no employee appears at the car manufacturer. Instead, however, at 2.02 p.m. the customs agent receives the export release electronically. In this case, the customs officer at the customs office of export did not consider it absolutely necessary to inspect the goods. The truck then drives to the Polish-Belarusian border over the next few days. There, Polish customs scans the export, which completes the process.

Summary of the two-stage procedure

In summary, the customs office of exit does not necessarily have to be a German customs office. The goods are declared at the inland customs office (customs office of export) and the released declaration is presented at the EU customs office of exit at the time of export. Export can be applied for via ATLAS if the value exceeds EUR 3,000. The export must be made in advance. Theoretically, this can also be done immediately by bringing the goods to the inland customs office. Alternatively, the goods can be inspected by customs at the consignor’s location (presentation outside the customs office).

Who can issue an export accompanying document?

The export accompanying document is usually issued by a customs agency or a forwarding agent. The customs agency then acts as the declarant’s representative vis-à-vis customs. It has special software for electronic declarations with a direct link to the customs offices. Manufacturers usually charge a one-off set-up fee for such a program, plus monthly basic fees and then transaction fees for each registration with the customs office.

Create the export accompanying document yourself

As an alternative to preparation by a customs service provider, the German Customs Administration also offers small companies and private individuals free preparation of the export accompanying document via the IAA website (Internet Export Declaration).

Technical requirements

To create the export yourself via the IAA’s free portal, you need a computer with a fast Internet connection. The user must have Java installed and an Internet browser that accepts cookies. In order to be able to display the finished export accompanying document in PDF format later, you also need a program that can display PDF documents. This can be, for example, “Adobe Reader” or equivalent free software.

Above all, however, it is important that you have a valid ELSTER certificate, i.e. a file in .pfx format. You can use this to log into the ELSTER portal and issue an ElsterOnline certificate to use the IAA Plus. The ElsterOnline certificate is valid as a signature and confirms that you have actually made the registration. You can find more information on the system requirements for ELSTER at: elster.de/system-requirements and directly on the page for using the “IAA Plus” portal: IAA Plus system requirements

As a company, you must also have an EORI number. If you do not yet have an EORI number, for example, you can apply for one here: Information on applying for an EORI number

Please note that you need the “TrueType font Code 128” on your computer to create and correctly display the export accompanying document. The document cannot be printed without this. You can download these directly from the IAA website or via Google search.

Preparation of documents

In the next step, you must make the following preparations to be able to create the ABD yourself:

- You need a document stating the nature of the transaction. It should state the value of the goods, the seller and the buyer or shipper/exporter and consignee

- You need to know which customs offices you need to specify in the declaration. This is the customs office of export at the place of the seller and the customs office of exit at the place where the goods leave the EU

- You know the weights (gross & net weight) of the individual types of goods and the entire consignment

- You know the number of packages in the shipment, if applicable

- If you ship commercially, you have an EORI number

- You know the customs tariff number of the respective goods and, if applicable, the export restrictions + additional codes for the customs declaration

Have you considered all of the above points on our checklist? You can then start preparing the export accompanying document:

Free creation of the export via IAA Plus

To create the ABD yourself, go to ausfuhrplus.internetzollanmeldung.de. The first helpful documents, such as a quick guide or the entire 230-page manual for the application, will then be directly available to you. After you have accepted the terms of use at the bottom of the page, you can continue to the login. After entering the EORI number + your branch number (if applicable) and selecting the certificate file, you will be logged in and taken to the start page of the application.

You can create a new export via the menu item “Customs office of export export declaration… normal procedure”. Please inform yourself about the one-stage procedure and the two-stage procedure before proceeding:

This is the basis for understanding the next steps and processes. From here you can use the IAA Plus help page for the remaining points: to the help page

Do you have any questions about creating the ABD? The Customs Service Desk will be happy to help you. You will find an overview of the hotline numbers on the following page: Internet Customs Registration Service Desk.

Are you still stuck? Or is creating your own too laborious for you? We will be happy to create your ABD. Contact us now.

What happens after the ABD has been created

Have you created and printed the ABD? This must now be passed on to your parcel service provider/forwarding agent. If you bring the goods to the border yourself, the ABD must be printed out with a legible barcode and brought to the customs office of exit. It is then scanned by the customs office, which creates the so-called exit note. You can pick up this exit note later in the IAA portal itself. It is proof that the goods have been properly exported from the customs union. The exporter of the goods should always keep the exit note for possible tax audits. This means that there is no tax liability when the goods are sold, as it is a tax-free export. Without valid proof, you could otherwise become liable for tax and have to pay 19% VAT retrospectively.

The German export accompanying document is the preliminary stage for Swiss import customs clearance. Goods must always be exported from one country before they can be imported into another country. Information on customs clearance: Switzerland can be found here.